I subscribe to several Twitter feeds. One is on higher education. A lot of posts with the #HigherEd tag are by institutions, but a fair number are by college students. Following their tweets is a good way for me to see what is on people’s minds and understand the challenges that college students face. It will surprise none of you that student loans and lending policies are a hot topic. They are even a hotter topic now that when I first posted this entry about a year ago.

Interest rates on unsubsidized student Stafford loans are high. Student loans are for ten years and currently carry a 6.8% rate. To put this into a comparative context, a twenty-year fixed rate home mortgage is at about 4%, a five-year auto loan at about 3.75%. And unlike your home or car loan, you can’t walk away from your student loan. Discharging a student loan in bankruptcy is extremely hard in part because the lender can’t repossess your education like it can your car or house. So it is important that you take a good hard look at the numbers when making the decision to finance your education through loans.

A little data can go a long way toward bringing some reality into your decision-making process. Table 1 reports median starting salaries and earnings at mid-career for people with different undergraduate majors. I want you to note two things: (1) there are big differences among majors. The typical chemical engineer earns more than twice as much after graduation than the typical child/family studies major; and (2) these differences get larger by the middle of careers because majors in the top part of the table enjoy much greater salary growth than majors in the bottom part of the table.

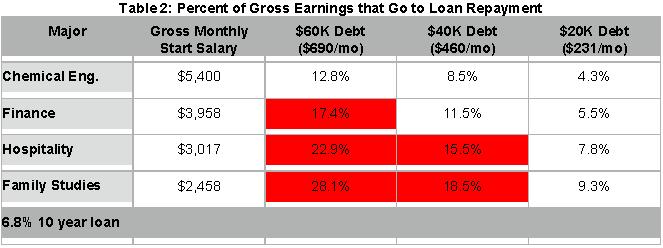

Table 2 shows why this is important. Here I have converted annual salaries to monthly figures for four different majors. I then assume these majors take out unsubsidized loans at 6.8%, accumulating $60K, $40K, or $20k of debt over four years. $20K of debt is about what you would accumulate at UNLV if you financed all of your tuition payments for four years through student loans. $60K is about the current aggregate limit on Stafford Loans for undergraduates.

The percentages in the table show how much of your gross monthly earnings from your first job would go just to repaying your student loan each month. So a chemical engineer who took out $60K would expect 12.8% of their gross monthly earnings to go to loan repayment. Notice that this is gross earnings–earnings before taxes. For a family studies major who took out $60K, that amount is 28%!! Yes, you can expect some growth in your income over time, but note that at mid-career the typical family studies major still isn’t making the starting salary of a finance major. A finance major who takes out $60K in loans is devoting almost twenty percent of their gross income just to student loan repayment. Notice you haven’t eaten, paid your rent, or put gas in the car yet. If you are a family studies major with $60K in debt, pray for inflation–it is a debtor’s friend.

Now, there is a fair bit of variance around the median numbers reported in Table 1. Some child and family studies majors, perhaps those that go to ivy league schools, will earn more than the typical graduate with the same degree. And, some chemical engineers, perhaps those who go to really bad schools will earn much less than the typical graduate. But, I seriously doubt that those ivy league family studies majors are going to earn anywhere near what the typical chemical engineer can expect upon graduation.

The bottom line is this: Getting a college degree is about much more than just dollars and cents, but some majors offer way bigger financial returns than others. If you believe that your future job will be the sole source of your ability to pay back your students loans (not your parents or a rich spouse), you want to do a calculation similar to this and ask yourself just how much of your expected income over the next ten years are you willing to devote to loan repayment. Some loan reform is coming that should lower rates, but keep in mind that experts suggest that no more than 10 to 15% of your starting salary should go to loan repayment. Someday soon, the government may do this for you by putting debt limits on student loans based on your expected earnings. Until then, it is up to you to determine just how much debt you are willing to take on to get the degree of your choice.

Paul Jarley, Ph.D., is the dean of the UCF College of Business Administration. He blogs every week at http://www.bus.ucf.edu/dean. This post appeared on February 20, 2013. Follow him on Twitter @pauljarley.