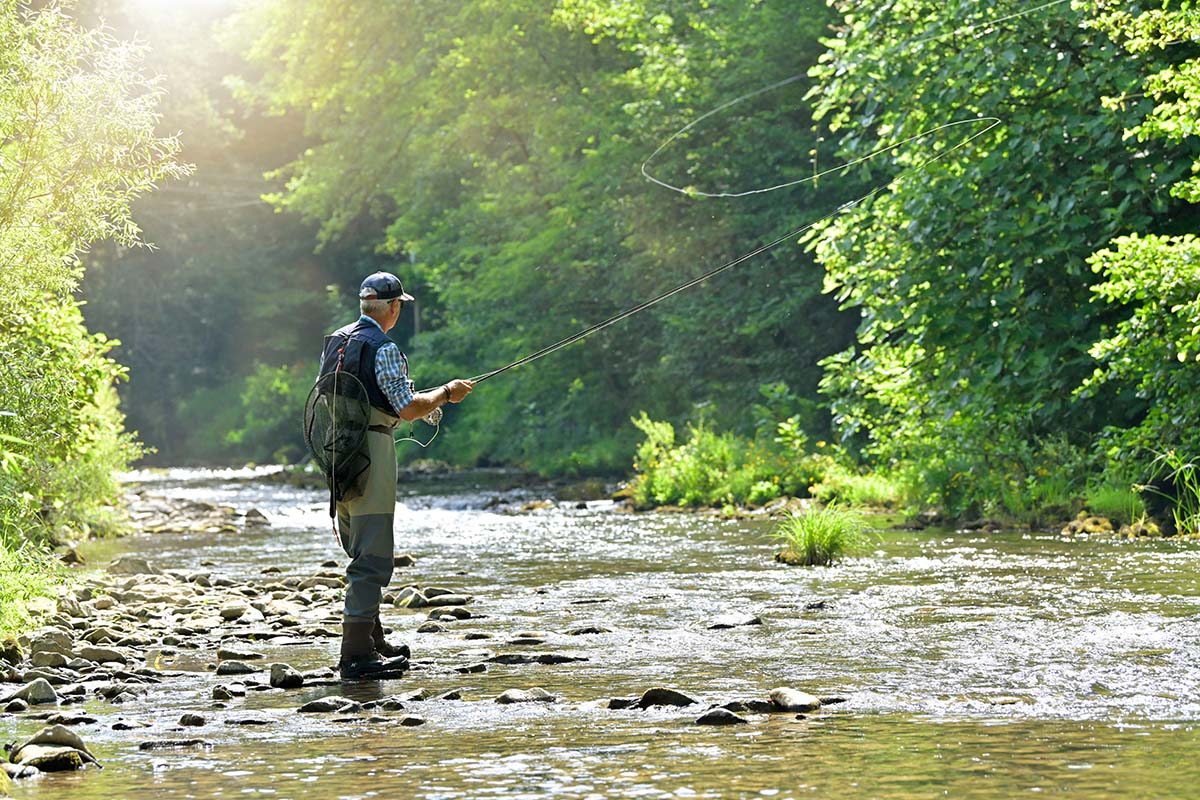

The latest U.S. economic forecast of Sean Snaith, the director of UCF’s Institute for Economic Forecasting and a nationally recognized economist in forecasting, analysis and market sizing, compares the trickiness of predicting a slowdown with the fickleness of fly fishing. In both, he says, indicators can give false signals.

“The economic indicators that were reliable signals of a recession in the past are giving false signals in the new economic riverbed forged by the pandemic policies,” Snaith says in his U.S. economic forecast released this morning.

Labor market and supply chain disruptions, massive monetary and fiscal stimulus, soaring energy prices and high inflation have at least temporarily altered the inner workings of the economy, says Snaith.

The results showed second-guessing, revised predictions and less confidence in the indicators that previously signaled economic slowdowns. Still, Snaith anticipates growth slowing in 2024 and unemployment rising. Job growth will slow to a trickle, he says, but should not turn negative.

Several additional highlights from Snaith’s four-year quarterly U.S. forecast include:

- Core consumer price inflation will continue its slow decline, but rising energy prices are likely to push the headline consumer price index higher in 2024. By the end of 2024, headline inflation will be close to the Federal Reserve’s target level of 2%, but the Fed has signaled that interest rate cuts could happen before this target is reached. This may prove to be a mistake.

- U.S. consumers powered the post-Covid recovery. Following the end of most lockdowns, consumers were ready to spend. But high energy prices, food costs and housing costs have steadily eroded their purchasing power. Credit card debt and drawing down savings have temporarily patched the hole in their monthly budgets, and this loss of purchasing power has set the table for the economic slowdown that is approaching.

- Despite resistance to the effects of Fed tightening thus far, the headline unemployment rate (U-3) is expected to gradually rise from 3.6% to 4.3% in 2027. The resiliency of the labor market has played a large role in keeping a recession at bay.

- The housing market remains tight. High prices combined with 7% mortgage rates have eroded demand. However, persistently low inventories will underpin the sector. Housing starts declined from 1.6 million in 2022 to 1.4 million in 2023 and will slowly ease, reaching 1.3 million in 2027.

- Higher interest rates and a presidential election will combine to suppress investment spending in 2024 and likely into 2025, and we expect spending to decelerate in both these years.

We are projecting national deficits through 2027 that will consistently average more than $1.75 trillion. The amount that the projected deficits will add to the national debt over the next four years will be $7 trillion, pushing the total national debt to more than $41.2 trillion and a debt-to-GDP ratio of nearly 130%. Slower-than-projected economic growth or a recession would also push projected deficits higher, though the possibility of faster-than-projected economic growth would help mitigate the growth of these deficits on the debt-to-GDP ratio.